How Race Shapes Retirement Security in an Aging America

- Jason M. Davis

- Mar 12

- 3 min read

Updated: Jun 3

Retirement savings are a core differentiator in economic security as people age. In the United States today, senior households without retirement income are three times as likely to live in poverty as those with retirement income.

As the US population ages, existing racial disparities in retirement savings levels threaten to increasingly divide economic security outcomes for older households.

The Retirement Income Gap

According to Chandan Economics' calculations using data from the US Census Bureau's American Community Survey, White, Multi-racial, and Black senior households are more likely to have retirement income than Native American, Asian, or Hispanic households.

48.2% of White, non-Hispanic senior households have retirement income, compared to 45.1% of multi-racial senior households, and 42.9% of Black senior households. Meanwhile, 37.8% of seniors who self-identify as "Other" have retirement income, compared to 35.7% of Asian seniors and 31.5% of Hispanic seniors.

We find that a notable White-black income gap remains despite Black Households having higher rates of savings compared to many other groups. Moreover, inequities in retirement security are intrinsically linked to earlier-in-life gaps in wealth accumulation and economic mobility.

Retirement Account Participation

Historically, income and job-related factors are strongly associated with disparities in the retirement account balances of older worker households.

A 2023 report by the Government Accountability Office, drawing on data from the Fed’s Survey of Consumer Finances (SCF) and surveys from the National Institute on Aging (NIA), found that higher-income households contributed a larger percentage of their pay than low-income households (about 8% and 5%, respectively). Higher-income households also received larger employer contributions.

Since Black and other minority households have disproportional shares of low-income prevalence relative to White households, they are also likely to contribute smaller shares of income towards retirement.

Moreover, White households and households without children enter retirement with significantly larger savings balances than minority or child-present households. Results from the GAO study showed that households of all races other than White and households with children had balances about 28% and 20% smaller, respectively.

The reasons for lower retirement account participation among low-income and minority adults can vary.

Previous research finds that, in some cases, low-income workers may not have the disposable income to participate in voluntary retirement programs because a large share of their earnings is used for essential goods such as food, clothing, or shelter.

Separate studies suggest that the structure of the US Social Security program may reduce incentives for low-income workers to participate in workplace retirement accounts when available.

While automatic enrollment has, in some cases, increased workplace account participation, it benefits only those with access to a workplace retirement account, and a substantial share of low-income workers lack this access.

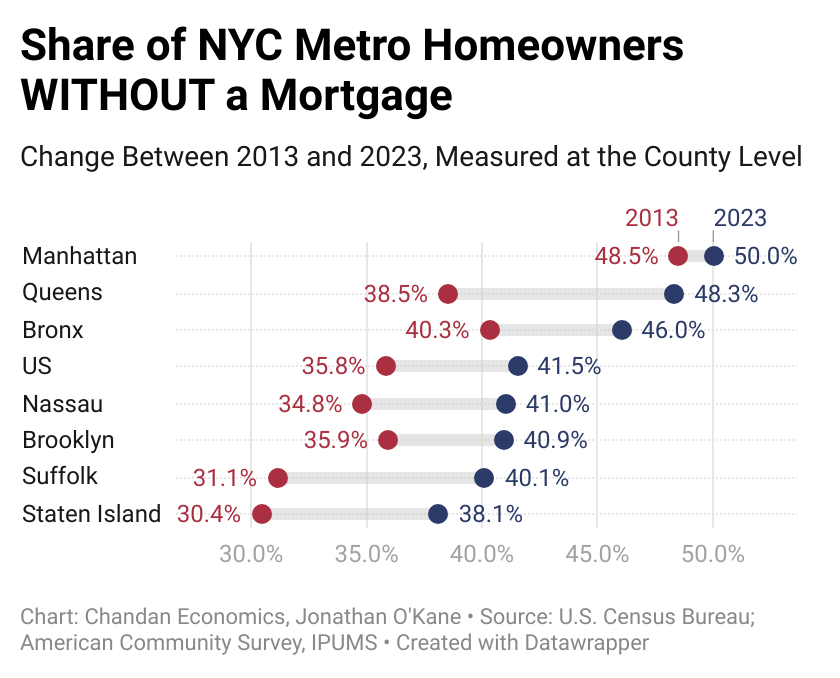

Homeownership and Wealth Accumulation

Homeownership disparities are also driving divides in retirement security. Roughly 7-in-10 White Households are homeowners, compared to roughly 6-in-10 Asian American or Pacific Islander Households (AAPI), and 5-in-10 Hispanic, Black, and Native American households.

Due to a peak in US homeownership rates in the early 2000s, baby boomers enjoy higher homeownership rates and larger wealth cushions upon entering retirement than previous generations.

However, with existing racial disparities in homeownership among the baby-boomer generation carrying over into the cohort's senior years, inequities in retirement security are taking a similar shape. 82% of White seniors are homeowners compared to 69% of Hispanic seniors, 66% of AAPI seniors, and 65% of Black seniors.

Looking Ahead

Ongoing racial disparities in income and wealth and their tendency to endure across a person’s lifecycle result in similar racial gaps in retirement security. As the US population ages and makes up a growing share of domestic housing demand, the dynamics of retirement security will increasingly shape the nation’s housing markets.

From a policy perspective, advancing access and participation in retirement programs among low-income and minority households is a crucial component of addressing these gaps, as is evening out demographic barriers to homeownership.

For our full analysis of racial inequities in US Housing, including implications for retirement security, read the full report here.

Comments